The United States wind energy sector is entering a period of significant acceleration, with new data projecting a 36% increase in wind installations for 2025 compared to the previous year. According to the latest U.S. Wind Energy Monitor report, a collaborative publication by Wood Mackenzie and the American Clean Power Association (ACP), the industry is expected to deploy more than 7 GW of new wind capacity in 2025. This surge marks a pivotal shift in the trajectory of American renewable energy, as the nation balances ambitious climate goals against a backdrop of complex economic headwinds and shifting energy demand.

While the immediate outlook for 2025 is optimistic, the industry remains in a delicate transition phase. The report maintains a five-year outlook of 46 GW of new wind capacity through 2029, a figure that remains unchanged from previous quarterly forecasts. However, the internal composition of this growth has shifted, with 2026 and 2027 emerging as the high-water marks for project commissioning.

Main Facts: A Sector in Transition

The wind industry’s growth is increasingly defined by a "back-loaded" installation pattern. Despite a slow third quarter in 2025, which saw installations fall 23% below initial forecasts to 932 MW, the pipeline for the final quarter is robust. Industry experts point to 3.8 GW of capacity currently queued for completion in Q4 2025, which would represent over half of the year’s total expected capacity. This is not an anomaly; rather, it reflects the typical, albeit demanding, project-commissioning timelines that govern large-scale infrastructure development.

A notable highlight in the report is the rebound in turbine order intake. After a period of stagnation, order volumes have returned to levels last seen before the enactment of the One Big Beautiful Bill Act (OBBBA). In the third quarter alone, the industry secured over 2 GW in firm commitments—a 79% increase quarter-over-quarter. This signals renewed confidence among developers, though the report cautions that "true visibility" into the market remains obscured as Original Equipment Manufacturers (OEMs) increasingly withhold granular project details, and a growing portion of "start-of-construction" activity is now conducted through off-site component manufacturing rather than traditional ground-breaking ceremonies.

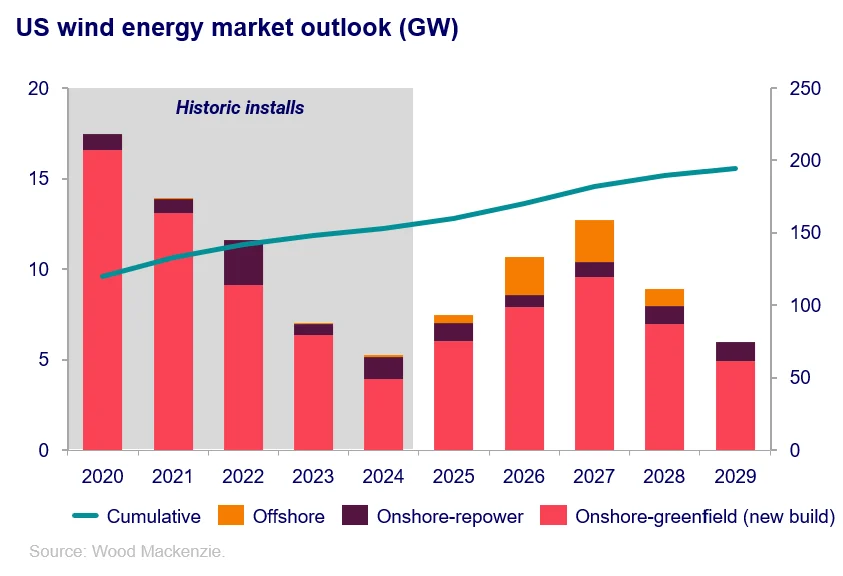

Chronology: The Path Toward 2029

The trajectory for U.S. wind energy is not uniform over the next five years; it is characterized by distinct peaks and valleys.

- 2025: The year of recovery and acceleration. With 7 GW of expected capacity, the market begins to shake off the inertia of the previous year.

- 2026: A banner year for the industry. Developers are expected to bring 10.7 GW online as major projects currently in the development pipeline reach operational status.

- 2027: The peak of the current five-year cycle. Projections indicate a substantial 12.7 GW of new capacity, driven by the commissioning of massive, long-term infrastructure projects.

- 2028-2029: A cooling-off period. The outlook for 2029 has weakened notably in the latest report. Analysts point to a rise in project cancellations and the designation of certain late-decade projects as "inactive." These setbacks are largely attributed to the persistent challenges of permitting, grid interconnection delays, and broader development hurdles that are currently stifling the long-term pipeline.

Supporting Data: The Drivers of Demand

The demand for wind energy is no longer driven solely by renewable portfolio standards or ESG mandates; it is being propelled by an unprecedented surge in power consumption. After a decade of flat electricity demand, the U.S. power market is facing a structural shift. Utilities have committed to 160 GW of large-load additions, a transformation necessitated by the rapid expansion of data centers and the broader electrification of the economy.

Data centers alone are projected to account for 59 GW of the 90 GW in total peak demand growth expected through 2029. With annual power demand growth now forecasted at 3%—a stark contrast to the 0.7% average of the previous decade—wind energy has found a new, vital role as a primary provider of clean baseload power. Wind’s competitive Levelized Cost of Energy (LCOE) makes it a natural fit for utilities and tech giants scrambling to secure reliable, cost-effective, and sustainable energy.

On the onshore front, the outlook is particularly stable. The three-year capacity forecast of 39.8 GW is fully committed, with turbine orders already placed for all scheduled projects. Western states—most notably Wyoming and New Mexico—are leading the charge, accounting for 34% of the projected growth. Landmark projects such as the 3.5-GW SunZia transmission and wind project in New Mexico and the 998-MW Towner Energy Center in Colorado highlight the scale of the current effort. Furthermore, the industry is seeing geographic diversification, exemplified by Arkansas commissioning its first utility-scale onshore wind project, the Crossover Wind farm.

Official Responses and Strategic Perspectives

Leila Garcia da Fonseca, Director of Research at Wood Mackenzie, notes that while the fundamentals are strong, the path forward is fraught with complexity.

"The U.S. power market is facing mounting strain," Garcia da Fonseca stated. "Wind energy benefits from strengthened economic fundamentals and a compelling business case driven by its competitively low LCOE. However, turbine costs remain elevated due to tariffs, and mid-term wind growth will depend entirely on our ability to resolve permitting and policy uncertainty."

The issue of tariffs is particularly contentious. The industry is currently grappling with a "scissor effect" where domestic manufacturing capacity is technically sufficient to meet demand, yet project costs continue to climb due to tariffs on raw material inputs and subcomponents. While Wood Mackenzie anticipates that turbine prices may moderate in the later years of the decade, onshore wind capital expenditure (CAPEX) is projected to rise by 5% through 2029, directly impacting the bottom line for developers and project owners.

Implications: Offshore Divergence and Future Risks

The offshore wind sector presents a more complex narrative of "diverging momentum." While projects like Vineyard Wind have demonstrated the capability to execute, connecting 15 turbines and delivering significant energy output in 2025, the broader sector is struggling.

The industry faces a severe constraint in the availability of specialized Wind Turbine Installation Vessels (WTIVs). This shortage, combined with harsh winter weather conditions that naturally limit construction windows, is pushing completion dates for several major offshore projects into 2026 and beyond. The report warns that for projects slated for post-2027 completion, the combination of financial pressure and logistical constraints could lead to further contract terminations and project delays.

Conclusion: Navigating a Complex Regulatory Landscape

The U.S. wind industry stands at a crossroads. The transition from a subsidy-driven model to a demand-driven model is well underway, with the surge in data center power needs providing a robust tailwind for future investment. However, the industry’s ability to meet the ambitious 46 GW target by 2029 will depend on two critical factors: the stabilization of the supply chain in the face of tariff-induced cost volatility and the aggressive reform of the permitting and interconnection processes that currently threaten the late-decade pipeline.

As the industry moves toward 2026 and 2027, the focus will shift from simple project announcements to the mechanics of execution. For policymakers, the challenge is clear: if the U.S. is to meet its rising power demand with clean, reliable wind energy, the current administrative and logistical barriers must be dismantled. Failure to do so risks leaving the nation’s growing energy needs unmet, while the successful resolution of these issues could solidify wind energy as the cornerstone of the American power grid for the next generation.